Rebuilding plan: Northern Shrimp (Pandalus borealis) - Shrimp Fishing Area 6

National Capital Region

- Date stock was determined to be at or below the limit reference point: 2017

- Date stock was prescribed to the Fish Stock Provisions: April 4, 2022

- Date Rebuilding Plan was approved: May 31, 2024

Foreword

In 2009, Fisheries and Oceans Canada (DFO) developed A Fisheries Decision-Making Framework Incorporating the Precautionary Approach (PA Policy) under the auspices of the Sustainable Fisheries Framework. It outlines the departmental methodology for applying the precautionary approach (PA) to Canadian fisheries. A key component of the PA Policy requires that when a stock has declined to or below its limit reference point (LRP), a rebuilding plan must be in place with the aim of having a high probability of the stock growing above the LRP within a reasonable timeframe.

In addition, under section 6.2 of the Fish Stocks provisions (FSP) in the amended Fisheries Act (2019), rebuilding plans must be developed and implemented for prescribed major fish stocks that have declined to or below their LRP. This legislated requirement is supported by section 70 of the Fishery (General) Regulations (FGR), which set out the required contents of those rebuilding plans and establish a timeline for each rebuilding plan’s development.

The purpose of this plan is to identify the main rebuilding objectives for Northern Shrimp in Shrimp Fishing Area (SFA) 6, as well as the management measures that will be used to achieve these objectives. This plan provides a common understanding of the basic “rules” for rebuilding the stock. This stock is prescribed in the Fishery (General) Regulations (section 69) and thus is subject to section 6.2 of the Fisheries Act and regulatory requirements.

The objectives and measures outlined in this plan are applicable until the stock has reached its rebuilding target. Once the stock is determined to be at the target, the stock will be managed through the standard Integrated Fisheries Management Plan (IFMP) or other fishery management process in order to fulfill the requirements of the FSP. Management measures outlined in this rebuilding plan are mandatory, and may be modified or further measures added if they fail to result in stock rebuilding.

This rebuilding plan is not a legally binding instrument which can form the basis of a legal challenge. The plan can be modified at any time and does not fetter the Minister's discretionary powers set out in the Fisheries Act. The Minister can, for reasons of conservation or for any other valid reasons, modify any provision of the rebuilding plan in accordance with the powers granted pursuant to the Fisheries Act.

Decisions flowing from the application of this rebuilding plan must respect the rights of Indigenous peoples of Canada recognized and affirmed by section 35 of the Constitution Act (1982), including those through modern treaties. Where DFO is responsible for implementing a rebuilding plan in an area subject to a modern treaty, the rebuilding plan will be implemented in a manner consistent with that agreement. The plan should also be guided by the 1990 Sparrow decision of the Supreme Court of Canada, which found that where an Aboriginal group has a right to fish for food, social and ceremonial purposes, it takes priority, after conservation, over other uses of the resource.

- Introduction and context

- 1.1 Biology of the stock

- 1.1.1 Larval dispersal

- 1.2 Environmental conditions and ecosystem factors affecting the stock

- 1.3 Fishery

- 1.4 Fisheries management challenges

- 1.5 Overview of the socio-economic and cultural importance of the fishery

- 1.5.1 Marine Stewardship Council Certification

- 1.5.2 Commercial fishery

- 1.5.3 Indigenous/special allocations

- 1.5.4 Processing and trade

- 1.6 Indigenous knowledge systems and contributions to the development of the rebuilding plan

- 1.1 Biology of the stock

- Stock status and stock trends

- Probable causes for the stock’s decline

- Measurable objectives aimed at rebuilding the stock

- Management measures aimed at achieving the objectives

- Socio-economic analysis

- Method to track progress towards achieving the objectives

- Periodic Review of the Rebuilding Plan

- References

Annex A: History of TAC levels and catch in SFA 6 (2013-2022)

Annex B: History of northern shrimp fishery

Annex C: Dependency analysis

Annex D: Exports of northern shrimp

Annex E: Membership - SFA 6 Rebuilding Plan Working Group

1.0 Introduction and context

This rebuilding plan is relevant to the Northern Shrimp (Pandalus borealis) fishery in Shrimp Fishing Area (SFA) 6, effective as of the 2024-25 fishing season. An Integrated Fisheries Management Plan (IFMP) is available for this stock as part of the IFMP for Northern Shrimp in SFAs 0,1,4-7 and the Eastern and Westerns Assessment Zones (EAZ and WAZ). The objectives and measures outlined in this rebuilding plan are applicable until the stock has reached its rebuilding target (see section 4.1). Once the stock is determined to be at the target, the stock will be managed through the IFMP. Where appropriate, this rebuilding plan refers to the IFMP for further information on the fishery.

1.1 Biology of the stock

Northern shrimp are found in the Northwest Atlantic from Baffin Bay south to the Gulf of Maine. Northern shrimp are typically found on soft and muddy substrates and in bottom temperatures ranging from 1°C to 6°C. However, the majority of Northern shrimp are caught in waters from 2°C to 4°C. These conditions typically occur at depths of 150 to 600 m and exist throughout the Newfoundland and Labrador offshore area. Northern shrimp represents the dominant shrimp resource in the Northwest Atlantic.

Northern shrimp are important prey for many species such as Atlantic cod (Gadus morhua), Greenland halibut (Reinhardtius hippoglossoides), redfish (Sebastes spp.), skates (Raja radiata, R. spinicauda), wolffish (Anarhichas spp.), and harp seal (Phoca groenlandica).

Northern shrimp are protandrous hermaphrodites; usually, they are born and first mature as males, mate as males for one or more years, and then change sex to spend the rest of their lives as mature females. During the daytime, Northern shrimp rest and feed on or near the ocean floor. At night, substantial numbers migrate vertically into the water column, feeding on zooplankton. Females produce eggs in the late summer-fall and carry the eggs until they hatch in the spring. There is no reliable method for aging shrimp in the field and growth is assumed to vary spatially and temporally based on environmental conditions. Fishable biomass (FB) is defined as the weight of all males and females with a carapace length greater than 17 mm. Most of the FB is female; however, the proportion of females in the fishable-sized survey catch varies by SFA and year.

While early genetic studies demonstrated that Northern shrimp in SFAs 4–6 are largely genetically homogenousFootnote 1, more recent preliminary research identified localized genetically-distinct pools that may be linked to smaller-scale oceanographic profiles (i.e., gyres). Recent preliminary research observed genetic differentiation in SFA 6, where reduced migration and gene flow was detected between inshore and offshore shrimpFootnote 2. These findings of genetic differentiation at the scale of this management unit show that although Northern shrimp have a larval phase, mechanisms of local retention and selection could affect the population structure in SFA 6. The assumption that locally depleted zones in SFA 6 could be replenished only by larval dispersion between management areas and within the area itself is highly unlikely.

1.1.1 Larval dispersal

It is recognized that Northern shrimp are distributed broadly over the Northwest Atlantic Ocean and that the SFA 6 management unit is biologically connected to adjacent areas through larval dispersal. Currently the rates of exchange (export/import) between these management units are unknown and rates of exchange of adults are less understood. The Labrador Current runs southward from SFA 4, through SFAs 5 and 6 and facilitates the transport of shrimp larvae. Larval dispersal simulation modeling within SFAs 4–6 indicated strong downstream larval connectivity and that a majority of recruits in a particular SFA may come from SFAs farther northFootnote 3. Northern shrimp larvae may travel several hundreds of kilometers before settlement and simulation modelling has demonstrated that larvae originating in the Arctic also show high potential settlement in SFAs 4–6. This research indicates low larval shrimp retention in SFAs 4 and 5, and higher larval retention in SFA 6Footnote 4.

1.2 Environmental conditions and ecosystem factors affecting the stock

Northern shrimp populations are influenced by various environmental and ecosystem conditions, including water temperature, prey availability and predation. As such, trends of such conditions are important to understand the current state and potential future trends of Northern shrimp.

The most recent information on the Newfoundland and Labrador Climate Index from 2022 indicated that 2021 was one of the warmest years on record, continuing the ongoing warming trend since 2018. The spring phytoplankton bloom was earlier than average in 2021, continuing a trend towards earlier blooms since the mid-2010s. The zooplankton community structure in recent years has returned to a state of higher proportion of larger copepod species (Calanus finmarchicus) which could potentially have a positive impact on energy transfer to upper trophic levels, of which Northern shrimp are a partFootnote 5.

Despite some positive signs in recent years (e.g. increased proportion of larger copepods), overall ecosystem conditions in the Newfoundland Shelf and Northern Grand Bank NAFO Divisions 2J3K (SFA 6, and southern part of SFA 5) remain indicative of overall limited productivity of the fish communityFootnote 6. While total biomass levels remain much lower than prior to the fish community collapse in the early-1990s, it showed some recovery up to the mid-2010s, when some declines where observedFootnote 7. Current total biomass (i.e., biomass of all fish functional groups combined) remains below the early-2010s level. Since the mid-2000s this fish community has shifted back to a finfish-dominated structure, but has shown small increases in shellfish dominance since 2018.

Under current ecosystem conditions (i.e., low shrimp stock sizes since 2015, low ecosystem productivity, shifting back to finfish dominated structure, low shrimp per-capita net production, and generally high predation pressure in SFA 6 and southern SFA 5) fishing is unlikely to be a dominant driver of shrimp stocks in SFA 6. Given the relative impact of predation in recent years in SFA 6 and southern SFA 5, small changes in catches have the potential to be more influential on stock trajectory than they may have been in the mid-2000s . See further discussion of predation and prey considerations in section 3.2.

1.3 Fishery

The shrimp fishery in SFA 6 is a directed, commercial fishery. The fishery occurs in Canadian Fisheries Waters adjacent to the Coast of Southern Labrador and Northern Newfoundland that lie north of latitude 49°15'N and south of 53°45'N, excluding the strait of Belle-Isle (Figure 1).

Despite linkages between the Northern shrimp populations managed in SFA 6 and more northern areas, the SFA 6 fishery is currently managed independently with Total Allowable Catch (TAC) set annually. TAC is the total amount of shrimp that is permitted to be caught for that fishing season. The fishing season in SFA 6 is April 1-March 31. There is no Northern shrimp fishery for food, social, ceremonial (FSC) or recreational purposes in SFA 6 (and the Northern shrimp fishery at large).

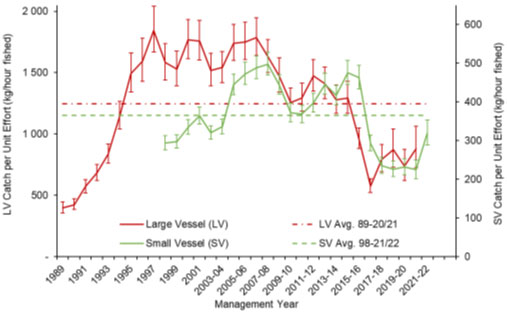

Annual TAC levels at the onset of this fishery in the late 1970s were less than 2,000 tonnes (t), harvested solely by the large-vessel (greater than 100 feet) fleet. The first substantial TAC increase occurred in 1994 to 11,050 t. commercial catch of Northern shrimp increased rapidly from the mid-1990s into the early-2000s within SFA 6 (Figure 2). TAC increases proceeded to the maximum historic TAC of 85,725 t in the 2008-09 fishing season. The resource was considered healthy and fisheries exploitation low (below 15 per cent)Footnote 8. TAC reductions have been applied periodically since 2009-10 due to stock declines which have been associated with changing oceanic conditions and increased abundance of shrimp predators.

Figure 2 - Text version

| Management Year | LV Modelled CPUE (kg/hour) | LV Lower 95% Confidence Intervals | LV Upper 95% Confidence Intervals | Average LV CPUE | SV Modelled CPUE (kg/hour) | SV Lower 95% Confidence Intervals | SV Upper 95% Confidence Intervals | Average SV CPUE |

|---|---|---|---|---|---|---|---|---|

| 1989 | 397 | 355 | 444 | 1247 | - | - | - | - |

| 1990 | 424 | 383 | 470 | 1247 | - | - | - | - |

| 1991 | 570 | 518 | 626 | 1247 | - | - | - | - |

| 1992 | 682 | 620 | 752 | 1247 | - | - | - | - |

| 1993 | 836 | 761 | 918 | 1247 | - | - | - | - |

| 1994 | 1147 | 1040 | 1266 | 1247 | - | - | - | - |

| 1995 | 1493 | 1343 | 1660 | 1247 | - | - | - | - |

| 1996 | 1595 | 1429 | 1780 | 1247 | - | - | - | - |

| 1997 | 1846 | 1669 | 2043 | 1247 | - | - | - | - |

| 1998 | 1582 | 1440 | 1738 | 1247 | 294 | 276 | 313 | 365 |

| 1999 | 1528 | 1395 | 1674 | 1247 | 297 | 281 | 315 | 365 |

| 2000 | 1767 | 1616 | 1932 | 1247 | 335 | 316 | 354 | 365 |

| 2001 | 1758 | 1604 | 1926 | 1247 | 364 | 343 | 387 | 365 |

| 2002 | 1520 | 1394 | 1657 | 1247 | 320 | 303 | 338 | 365 |

| 2003-04 | 1542 | 1420 | 1674 | 1247 | 336 | 318 | 355 | 365 |

| 2004-05 | 1741 | 1599 | 1895 | 1247 | 444 | 419 | 471 | 365 |

| 2005-06 | 1752 | 1607 | 1910 | 1247 | 473 | 445 | 502 | 365 |

| 2006-07 | 1786 | 1639 | 1947 | 1247 | 489 | 460 | 519 | 365 |

| 2007-08 | 1630 | 1500 | 1771 | 1247 | 498 | 469 | 528 | 365 |

| 2008-09 | 1475 | 1342 | 1621 | 1247 | 445 | 420 | 471 | 365 |

| 2009-10 | 1257 | 1149 | 1374 | 1247 | 372 | 349 | 396 | 365 |

| 2010-11 | 1295 | 1186 | 1414 | 1247 | 368 | 347 | 391 | 365 |

| 2011-12 | 1473 | 1351 | 1606 | 1247 | 398 | 374 | 423 | 365 |

| 2012-13 | 1410 | 1287 | 1544 | 1247 | 446 | 419 | 474 | 365 |

| 2013-14 | 1278 | 1167 | 1399 | 1247 | 417 | 393 | 443 | 365 |

| 2014-15 | 1291 | 1167 | 1429 | 1247 | 475 | 445 | 507 | 365 |

| 2015-16 | 960 | 880 | 1048 | 1247 | 463 | 434 | 495 | 365 |

| 2016-17 | 576 | 523 | 634 | 1247 | 293 | 273 | 314 | 365 |

| 2017-18 | 794 | 691 | 912 | 1247 | 235 | 215 | 257 | 365 |

| 2018-19 | 871 | 728 | 1042 | 1247 | 226 | 207 | 247 | 365 |

| 2019-20 | 737 | 621 | 875 | 1247 | 232 | 212 | 253 | 365 |

| 2020-21 | 878 | 724 | 1064 | 1247 | 225 | 202 | 250 | 365 |

| 2021-22 | - | - | - | - | 319 | 288 | 353 | 365 |

| * Included are the mean LV and SV of CPUE series. | ||||||||

A history of TAC levels and catch in SFA 6 (2013-2022) is available in Annex A. TAC levels were set with potential ER in the range of 19-22 per cent from 2013 to 2016 as the stock declined into the Cautious Zone. Since the SFA 6 stock entered the Critical Zone in 2017-18, based on the 2016 survey, the ER has been maintained at a maximum of 10 per cent of the estimated FB, consistent with the 2018 rebuilding plan for this stock.

Further details on fishery history, characteristics and management measures are available in the IFMP sections 1 and 7.

1.4 Fisheries management challenges

1.4.1 Suitability of the Limit Reference Point (LRP)

The upper stock reference (USR) and LRP for Northern shrimp in SFA 6 were developed through a combination of non-peer review (working group) and scientific peer-review processes and defined based on the geometric mean of the female spawning stock biomass (SSB) index over a period from 1996-2003 (see section 2.0). Work to develop these reference points considered findings of the Precautionary Approach (PA) Workshop on Canadian Shrimp and Prawn Stocks and Fisheries in 2008Footnote 9.

Since the reference points were developed, there have been changes in environment, ecosystem and predation; factors that can have negative impacts on Northern shrimp. All industry stakeholders have expressed concern that the LRP in SFA 6 is inappropriate given that the reference period coincides with a period of record low biomass of shrimp predators in the region. Moreover, stakeholders have highlighted the rapid increase, or “surge” in shrimp biomass following the collapse of groundfish predator biomassFootnote 10. Previous scientific review of the changes in shrimp biomass during this period suggest a great deal of uncertainty regarding the extent of growth in the shrimp population. As such it cannot be quantified using current data.

As a result, a Canadian Science Advisory Secretariat (CSAS) Science Response Process was held in January 2017 to review the reference points used in the PA framework for Northern shrimp in SFA 6. The resulting Science Response ReportFootnote 11 concluded that despite the decline in shrimp per‑capita net production, resulting from changing environmental and ecosystem factors, there was not enough information to determine whether shrimp are experiencing a new productivity regime, and it was not yet clear whether there were low or high productivity regimes in the past. These concerns are consistent with survey, catch rates and indices developed from shrimp predator stomachs for the period prior to the current RV time series, which begins in 1996. Further, biomass needed to support other resources in the current state of the ecosystem (i.e. the role of shrimp as a forage species) would also need to be assessed in the consideration of revised reference points.

The peer-review process concluded that it did not have sufficient evidence to recommend alternative interim reference points as a result of the January 2017 meeting and is of the view that, given high level of uncertainties and the importance of shrimp to other species as a forage species, lowering the current biomass reference points would involve a high amount of risk to the ecosystem and to the resource. It was concluded that the current biomass reference points used in the Northern shrimp PA would remain unchanged until additional information and / or analyses were available.

1.4.2 Development of a population projection model

A CSAS Regional Peer Review was held in May 2019 to develop a new PA Framework for Northern shrimp in the Newfoundland and Labrador Region. The key objective of this meeting was to review proposed population models and define LRPs, consistent with the PA, for Northern shrimp in SFAs 4-7. A shrimp population model incorporating environmental and ecosystem drivers was developed and peer reviewed during the CSAS meeting. The model utilized North Atlantic Oscillation (NAO) and predation by Atlantic cod (Gadus morhua), Greenland halibut (Reinhardtius hippoglossoides), and redfish (Sebastes spp.) to predict productivity changes within SFAs 4-7, permitting a prediction of total biomass in the following year. While the model was accepted, the consensus from the reviewers and meeting participants determined that the model was inappropriate for management decision-making.

During this meeting, historical biomass estimates of Northern shrimp reconstructed from historical shrimp surveys and diet analyses were presented. Although meeting participants agreed that three different data sources showed a dramatic increase in Northern shrimp biomass during the early 1990s, the estimate of population increase, and therefore, the precise biomass estimates and the proposed LRP developed from the rate of increase were deemed inappropriate for management use. As a result, the provisional SFA 6 LRP from 2010, which was considered the best available evidence, was retained for management use until such a time that alternative reference points are developedFootnote 12.

The absence of a population projection model presents a significant limitation in the management of the stock in SFA 6, and the Northern shrimp fishery at large. There is currently no ability to predict how fishing pressure and changing environmental conditions may affect future shrimp abundance in SFA 6, in the short or long term. Work to develop a model for use in assessing the SFA 6 stock is ongoing. DFO Science considers the development of a population projection model a crucial next step in the process to review PA reference points and is tentatively scheduled for CSAS peer-review in Fall 2024.

1.4.3 Spatial scale of shrimp science assessment and management units

SFAs were created to distribute fishing effort and improve the effectiveness of management regimes in the Northern shrimp fishery. The resulting management boundaries are, to some extent, arbitrary and selected based on factors other than species population structure. The stock assessment for Northern shrimp in SFA 6 is conducted at the management unit scale to accommodate fisheries management/industry preferences and historic practices. However, the biological stock unit for Northern shrimp is recognized to be larger than the current management scales. For this reason, DFO Science has advised that caution in interpreting and applying stock status information at sub-stock scales (e.g., SFA scale) is warranted. Despite acknowledgment of this limitation, stock assessment and management still occur at the SFA level for the time being.

Understanding Northern shrimp resource dynamics as a whole requires integrating information from all assessment areas. Work is ongoing to improve our understanding of Northern shrimp population dynamics that could be used to inform the spatial scale of biological reference points and formal stock assessment in the future, that are potentially better aligned with units of production.

Additional management issues, not specific to the SFA 6 fishery, are in IFMP section 4.

1.5 Overview of the socio-economic and cultural importance of the fishery

The Northern shrimp fishery in SFA 6 makes an important contribution to Newfoundland and Labrador as well as the regional economy through income, employment and the use of operational goods and services in the supply chain from harvesting to processing, to distribution and export. Northern shrimp is harvested by two fleets; the less than 89 feet 11 inches inshore fleet and the greater than 100 feet offshore fleet.

The Northern shrimp fishery began in the early to mid-1970s following exploratory cruises by DFO that confirmed the presence of shrimp in the waters from Baffin Island southward to Newfoundland and Labrador. By the late 1980s, the Northern shrimp fishery had developed into a substantial industry with capital-intensive investments in modern freezer trawlers and annual landings of over 26,000 t. In the mid-1990s, significant growth in the biomass led to the introduction of the inshore fleet and special allocation holders. The Northern shrimp TAC in SFAs 0 to 7 continued to increase, and by 2008-09, it had peaked at about 177,000 t, of which the SFA 6 TAC accounted for about 85,725 t, or close to 50 per cent. Subsequent to 2008, shrimp quotas in SFA 6 started to decline. By 2015, TAC reached 48,196 t (about a 44 per cent reduction over that seven year period) and declined further, reaching 9,430 t in 2022-23 (subsequently rolled over in 2023-24). Further details on the history of the fishery are at Annex B.

In the 2019 paper, Carruthers et al.Footnote 13 indicate that socio-economic impacts of the shrimp fishery are broadly distributed throughout the province of Newfoundland and Labrador. The paper highlights the importance of the fishery on employment in processing sectors and other related businesses. It also notes that there is significant spending of harvesters on fuel and supplies and services needed for fishing and shows that there are economic spillover effects of shrimp harvesting activities that are important for the maintenance of community infrastructure.

1.5.1 Marine Stewardship Council Certification

As a component of the broader Canadian Northern shrimp fishery, the fishery in SFA 6 was certified to the Marine Stewardship Council (MSC) standard in 2008. The MSC is an international non-profit organization established to promote sustainable fisheries and runs the most widely recognized environmental certification and eco-labeling program for wild capture fisheries. The fishery is assessed against three core MSC Principles and Criteria for Sustainable Fishing: sustainable fish stocks, minimizing environmental impact, and effective fisheries management.

1.5.2 Commercial fishery

In 2021-22Footnote 14, the SFA 6 quota represented 12 per cent of the overall Northern shrimp TAC (in SFAs 0, 1, EAZ, WAZ, 4, 5 and 6). The SFA 6 quota of 9,534 t was divided according to established per cent shares (see IFMP section 6.3): 6,636 t to inshore licence holders shared between the 2J, 3K north, 3K south, 3L and 4R fleets; 2,202 t to offshore licence holders; and 696 t to special allocation holders.

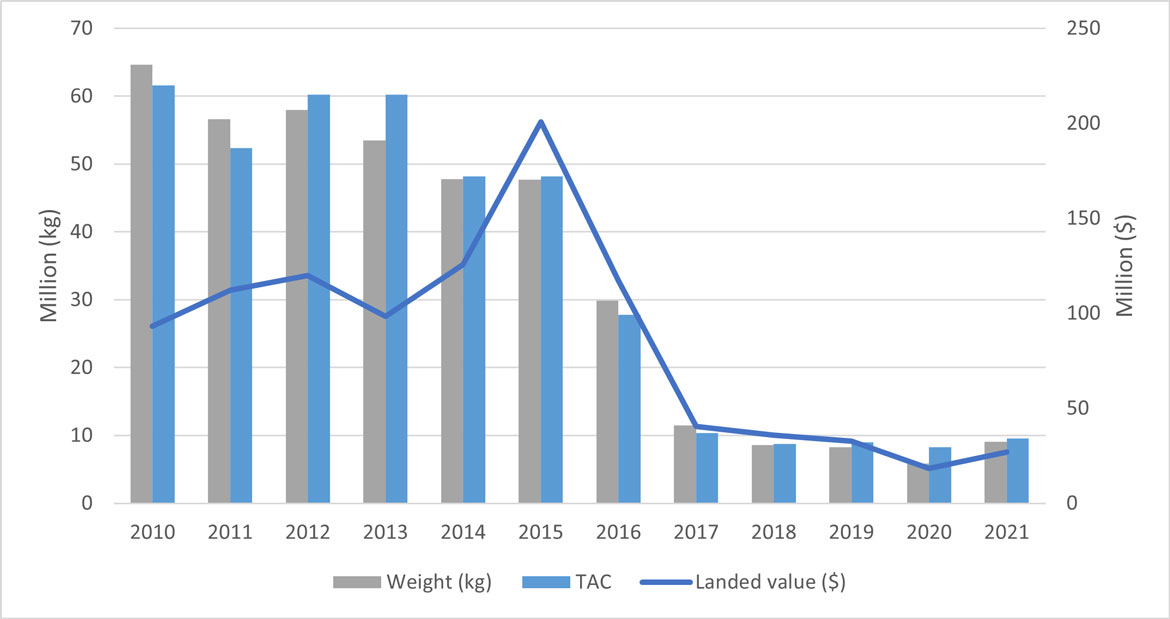

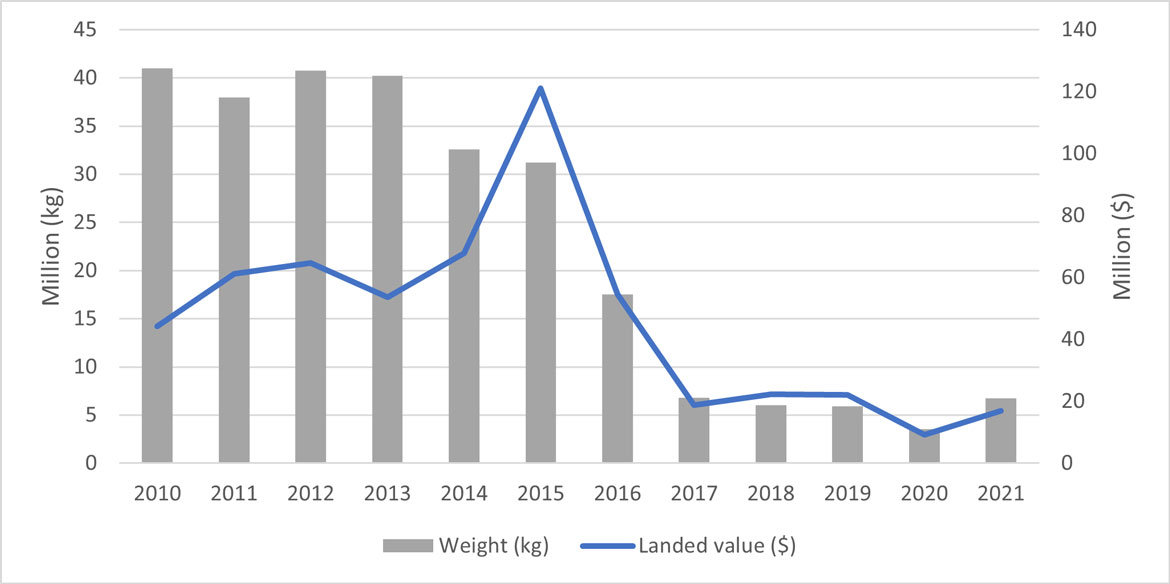

Figure 3 - Text version

| Year | Weight (Million kg) | TAC (Million kg) | landed value (Million $) |

|---|---|---|---|

| 2010 | 64.6304 | 61.632 | 93.12098 |

| 2011 | 56.66019 | 52.387 | 112.2806 |

| 2012 | 57.99478 | 60.245 | 119.8509 |

| 2013 | 53.50618 | 60.245 | 98.41545 |

| 2014 | 47.7952 | 48.196 | 125.6397 |

| 2015 | 47.67303 | 48.196 | 200.8891 |

| 2016 | 29.88281 | 27.825 | 117.3429 |

| 2017 | 11.49363 | 10.4 | 40.50362 |

| 2018 | 8.613865 | 8.73 | 36.00358 |

| 2019 | 8.254862 | 8.96 | 32.65807 |

| 2020 | 5.849908 | 8.29 | 18.51569 |

| 2021 | 9.117058 | 9.534 | 26.9863 |

As shown in figure 3, the Northern shrimp fishery experienced a substantial growth in terms of landed value in the mid-2010s supported by high landed prices, which was followed by significant declines in recent years. An annual landed value for the 2011-2015 period averaged $125 million, which declined to an average of $46 million for the 2016-2021 period. In 2021, total landings of Northern shrimp from SFA 6 amounted to 9.1 thousand tonnes valued at $27.0 million, which represented 16 per cent of total Northern shrimp landings from all SFAs by volume, and 14 per cent by landed value.

1.5.2.1 Inshore fleet

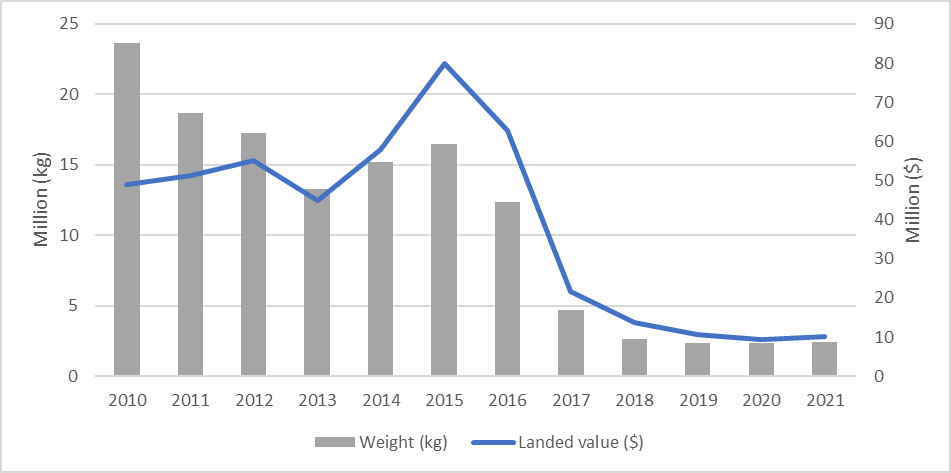

In 2021, there were 138 licence holders/enterprises that participated (i.e., were active with landings) in the inshore Northern shrimp fishery in SFA 6. This number has declined by more than 50 per cent compared to 2012. In 2021, these 138 licence holders caught approximately 6,712 t of Northern shrimp with a landed value of about $16.9 million . Figure 4 shows the time trend of inshore landed volume and landed value of SFA 6 shrimp which has been generally following the same trends as overall Northern shrimp landings in SFA 6. That is, high volume and increasing landed value of Northern shrimp landings in 2010-2015 followed by a sharp decline of both landings volume and landed value from 2015 onwards. Despite a small uptick in landed volume and value in 2021, overall, the performance of Northern shrimp in SFA 6 has been low over the 2017-2021 period.

In 2021, the 138 inshore license holders harvested a total of 25,086 t of all species from all fishing areas with a total landed value of approximately $161.9 million. Other species harvested by these enterprises were primarily snow crab ($112.8 million or 77 per cent of the total landed value), and shrimp from outside of SFA 6 ($9.8 million or 7 per cent).

The average fishing revenue dependency on SFA 6 Northern shrimp for these inshore enterprises was 17.5 per cent in 2021. The majority of these enterprises (71 out of 138, or 51 per cent) had a dependency on SFA 6 Northern shrimp ranging from 10 to 25 per cent. There were only a few enterprises whose fishing revenue dependency on SFA 6 Northern shrimp was greater than 50 per cent. See Annex C for the details of the dependency analysis for the inshore fleet.

Figure 4 - Text version

| Year | Weight (Million kg) | landed value (Million $) |

|---|---|---|

| 2010 | 40.970079 | 44.25849358 |

| 2011 | 37.976088 | 61.11485133 |

| 2012 | 40.751321 | 64.69104719 |

| 2013 | 40.236661 | 53.55773946 |

| 2014 | 32.573364 | 67.79729584 |

| 2015 | 31.208782 | 121.0936536 |

| 2016 | 17.550639 | 54.55446271 |

| 2017 | 6.775595 | 18.76422812 |

| 2018 | 6.000304 | 22.22240461 |

| 2019 | 5.896446 | 22.01034048 |

| 2020 | 3.523203 | 9.16550458 |

| 2021 | 6.711852 | 16.92789441 |

The majority of the inshore shrimp enterprises based in 2J3KL have access to snow crab. In 2021, 95 of the 138 enterprises, which are based in 2J3KL, harvested snow crab with an average landed value per enterprise of about $1.2 million. However, the 4R shrimp fleet, which includes 41 enterprises, does not have access to snow crab. As a result, approximately 92 per cent of their total landed value is obtained from shrimp. Specifically, the vast majority of these enterprises have access to two shrimp areas, SFA 6 and SFA 8 (Esquiman Channel). Of their total landed value, 68 per cent is derived from SFA 8 Northern shrimp, while SFA 6 Northern shrimp contributes about 24 per cent.

Due to these differences in access to species other than shrimp, dependency ratios for the 4R and 2J3KL fleets differ. On average, fishing revenue dependency on SFA 6 shrimp is higher for the 4R fleet (average dependency of 25.7 per cent) than for the 2J3KL fleet (average dependency of 13.9 per cent). Annex C provides more details on the dependency ratio calculations for these two fleet groupings.

1.5.2.2 Offshore fleet

Vessels with a length greater than 100 feet are categorized as part of the offshore fleet. In 2021, out of the 17 licences issued for offshore harvesting of SFA 6 Northern shrimp, seven enterprises caught a total of 2,405 t of Northern shrimp from SFA 6 valued at $10.0 million. Figure 5 shows the time trend of SFA 6 Northern shrimp landings for the offshore fleet.

The offshore enterprises harvested a total of 40,884 t of all species from all regions valued at $162.9 million. Other species caught by these seven enterprises are Northern shrimp from other SFAs ($92.6 million or 57 per cent of the total landed value), striped shrimp ($24.2 million or 15 per cent), Greenland halibut ($19.0 million or 12 per cent), and sea scallop ($13.5 million or 8 per cent).

The average landed value for these seven offshore enterprises (from all the species) was $23.3 million per enterprise, of which the average landed value of $1.4 million corresponded to Northern shrimp from SFA 6. The average fishing revenue dependency of these offshore enterprises on SFA 6 Northern shrimp was 9.8 per cent in 2021. Only 2 out of 7 enterprises had a dependency on SFA 6 Northern shrimp greater than 10 per cent, both within the range of 10-50 per cent.

1.5.2.3 Employment

It is difficult to estimate employment information specific to the SFA 6 Northern shrimp fishery as harvesting fleets and processors’ operations are dependent upon other species as well as harvests from other regions. However, it is estimated that approximately 700 crew members (defined as licence holders plus hired harvesters) participated in the inshore SFA 6 Northern shrimp fishery in 2021Footnote 15. Additionally, according to a survey from the Canadian Association of Prawn Producers members in 2016, there are 530 year-round offshore crew employed in shrimp fishing in Newfoundland and Labrador region.Footnote 16 It is also estimated that approximately 700 workers are employed in the onshore fish processing plants that process shrimp (see section 1.5.3).

1.5.3 Indigenous/special allocations

Since the late 1970s, the Northern shrimp fishery has included licences held by Indigenous birthright corporations and other community-based organizations owned predominately by Indigenous peoples. Beneficiaries of these licences included residents of Labrador, Quebec, and Nunavut. The revenue generated from this access, whether through direct fishing or royalty charter arrangements, has contributed to economic development and employment within these communities.

There are currently three communal commercial licences in the inshore sector in SFA 6 and one communal commercial licence in the offshore sector. There is no FSC fishery for Northern shrimp.

Including the offshore communal commercial licence, there are 6.5 offshore commercial licences held by Indigenous interests. Also, Innu Nation is one of the three special allocation holders and primarily transfers the allocation to the offshore fleet through royalty arrangements.

There are three special allocations holders operating in SFA 6. Special allocations are typically harvested by the offshore fleet through royalty arrangements. However, there is no readily available information about this group that would allow an estimate of the royalty they earn from leasing their quota, or the degree of dependency on this income.

1.5.4 Processing and trade

1.5.4.1 Processing

In addition to the harvesting sector, the Northern shrimp fishery in SFA 6 also supports processing plants and provides important local employment, most notably in Newfoundland and Labrador. Currently, there are 64 fish processing companies in Newfoundland and Labrador operating a total of 89 onshore processing plants. Of the eight primary shrimp processing licence holders, six reported shrimp production in 2021 with two processing solely shrimp. It is estimated that these active shrimp primary processing plants employ approximately 700 processing workers. These employment estimates represent all shrimp processors in Newfoundland and Labrador sourcing raw material from multiple areas including the Gulf of St. Lawrence, with shrimp from the SFA 6 inshore fleet accounting for a large proportion.

1.5.4.2 Trade profile

Current available trade datasets do not allow for tracking of the source of catch by SFA; it is therefore impossible to identify the fishing area where the final product originated. Given this data limitation, and considering that SFA 6 makes an important contribution to the Newfoundland and Labrador onshore shrimp processing sector, being the main source of materials, as well as the offshore sector, this plan presents the total shrimp export from Newfoundland and Labrador only to provide a profile of the export trend, the main product types exported, and major marketsFootnote 17.

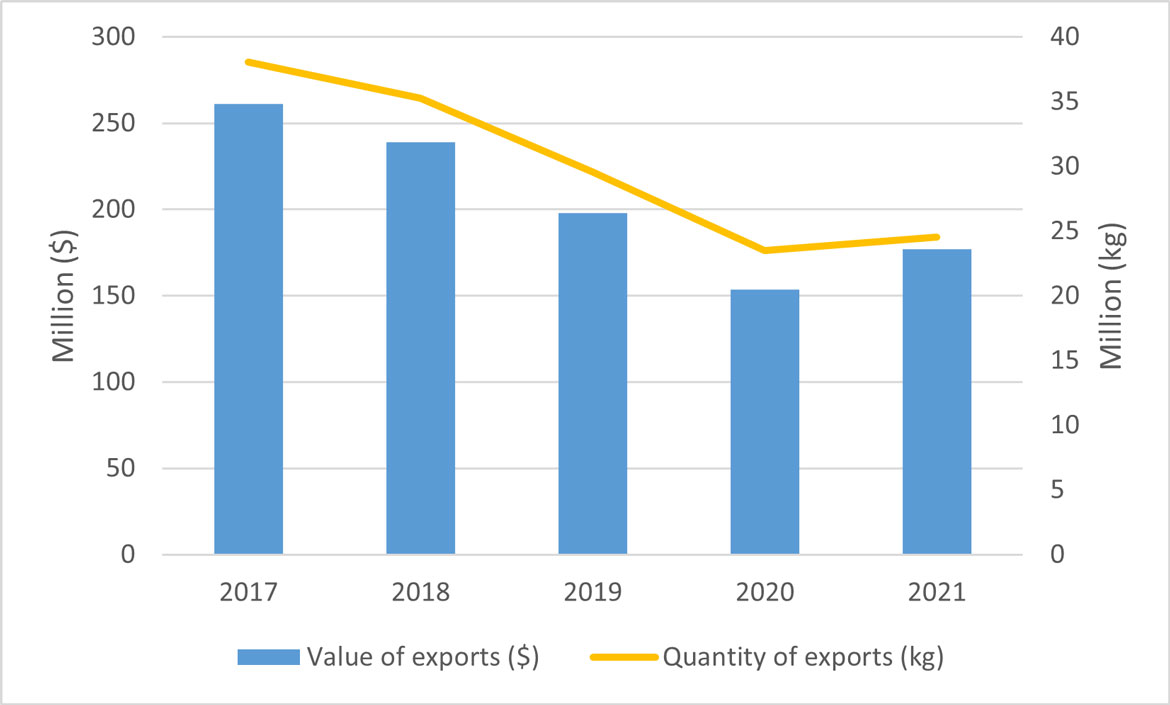

A total of 24.5 thousand tonnes of Northern shrimp was exported from Newfoundland and Labrador valued at 177 million in 2021. Total Northern shrimp exports from Newfoundland and Labrador have been following a general downward trend since 2017, despite a slight increase in export volume and value in 2021 (Figure 6).

Figure 6 - Text version

| Year | Value of exports ($) | Quantity of exports (kg) |

|---|---|---|

| 2017 | 261017514 | 38064435 |

| 2018 | 239164580 | 35249977 |

| 2019 | 198114026 | 29579864 |

| 2020 | 153391143 | 23488616 |

| 2021 | 177109625 | 24527736 |

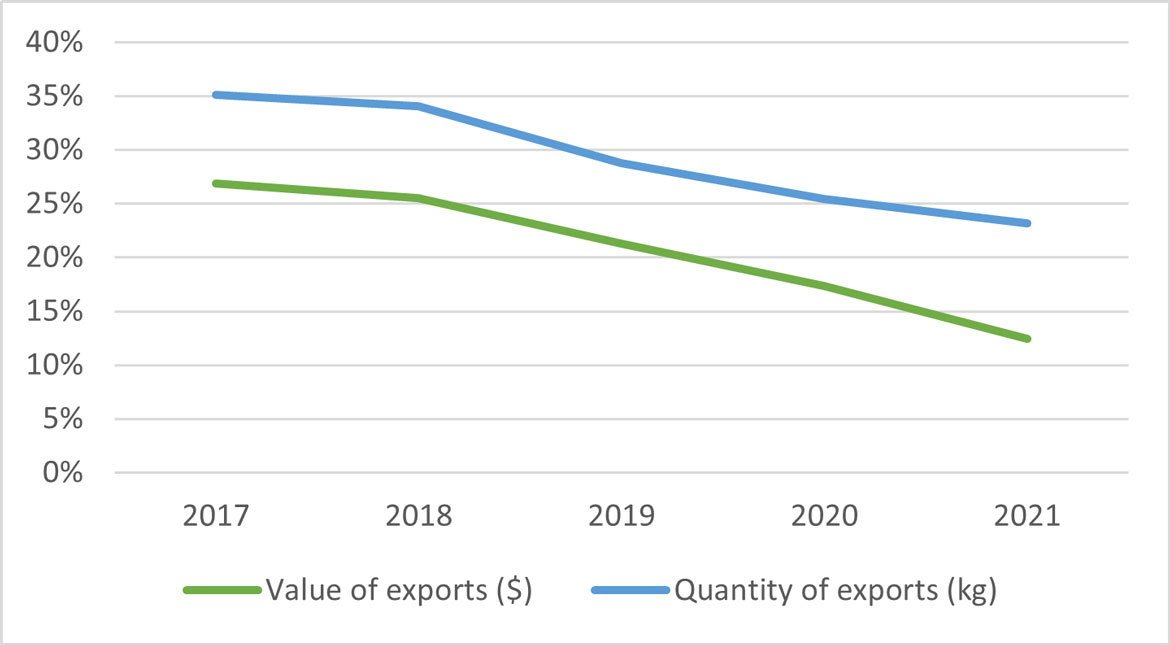

In 2021, Northern Shrimp exports represented 12 per cent of Newfoundland and Labrador total fish and seafood exports by value. The importance of shrimp as a proportion of total exports has been declining over the course of the last 5 years (2017 – 2021), from about 26 per cent to 12 per cent of total Newfoundland and Labrador export value (Figure 7).

Figure 7 - Text version

| Year | Value of exports ($) | Quantity of exports (kg) |

|---|---|---|

| 2017 | 27% | 35% |

| 2018 | 26% | 34% |

| 2019 | 21% | 29% |

| 2020 | 17% | 25% |

| 2021 | 12% | 23% |

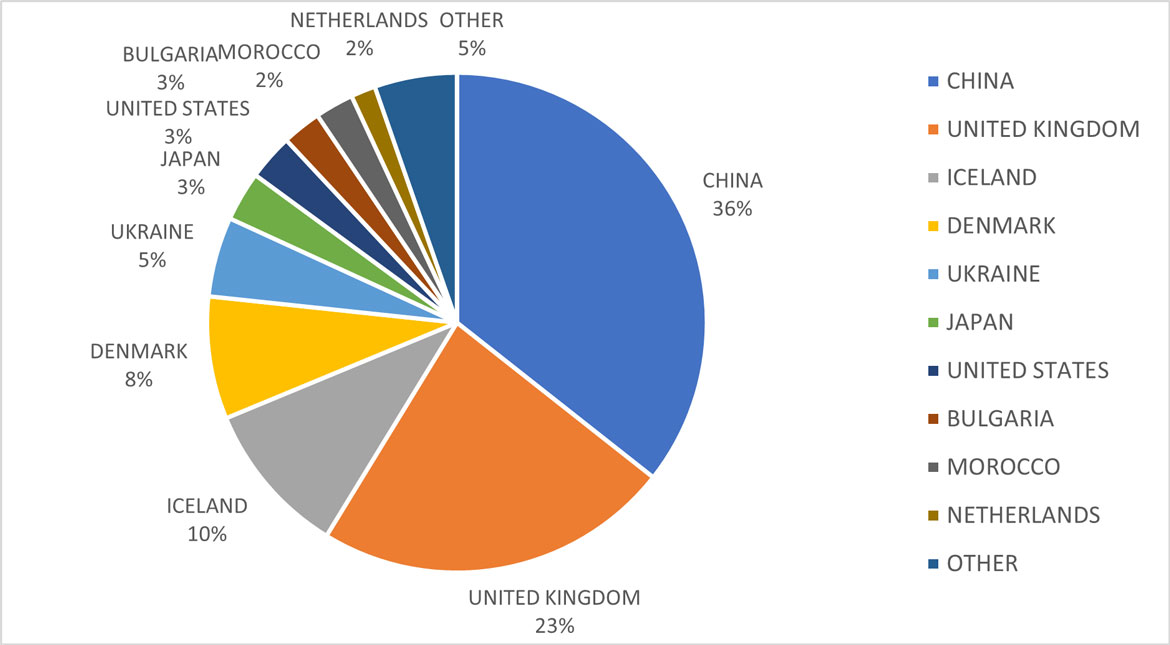

The main export destinations for shrimp from Newfoundland and Labrador are China (36 per cent of all shrimp export value in 2021), United Kingdom (23 per cent) and Iceland (10 per cent) (see Figure 8).

Figure 8 - Text version

| Export Destination | Export value |

|---|---|

| China | 36% |

| United Kingdom | 23% |

| Iceland | 10% |

| Denmark | 8% |

| Ukraine | 5% |

| Japan | 3% |

| United States | 3% |

| Bulgaria | 3% |

| Morocco | 2% |

| Netherlands | 2% |

| Other | 5% |

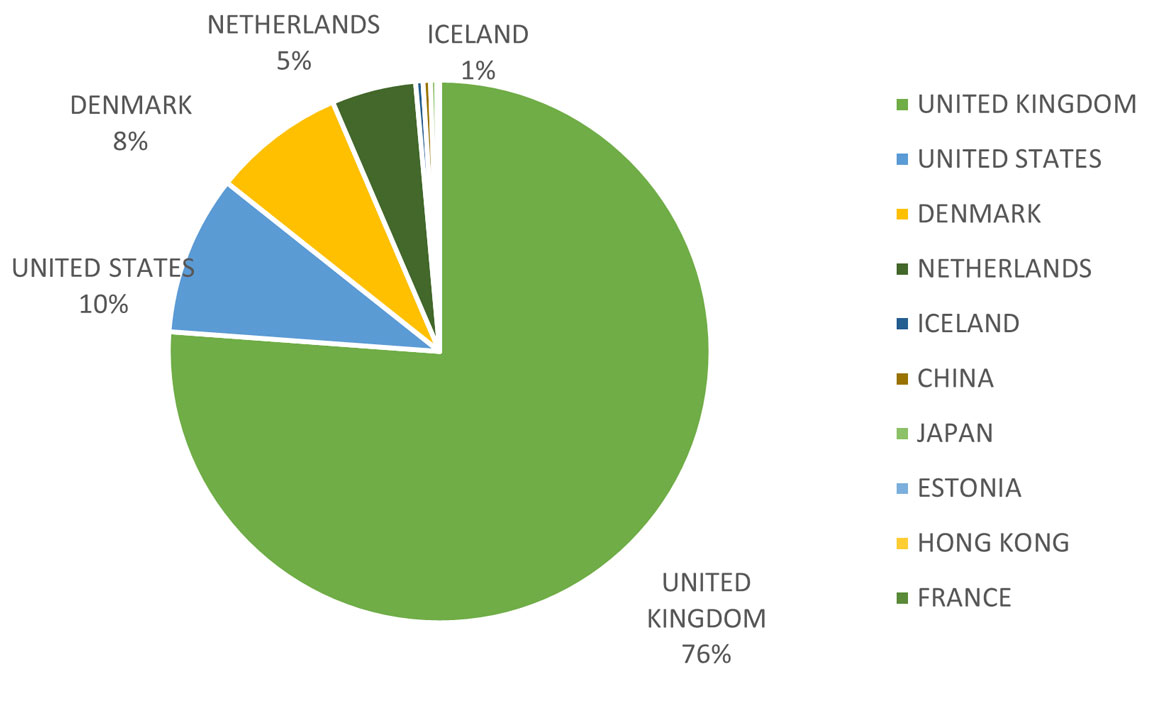

Landings from the inshore fleet are processed onshore mainly for the cooked and peeled market. In 2021, the export of cooked and peeled Northern shrimp from Newfoundland and Labrador was 5.2 thousand tonnes valued at $53 million. Major destinations for these products are the United Kingdom, the United States, and Denmark accounting for 76 per cent, 10 per cent and 8 per cent respectively, of total cooked and peeled shrimp export value in 2021.

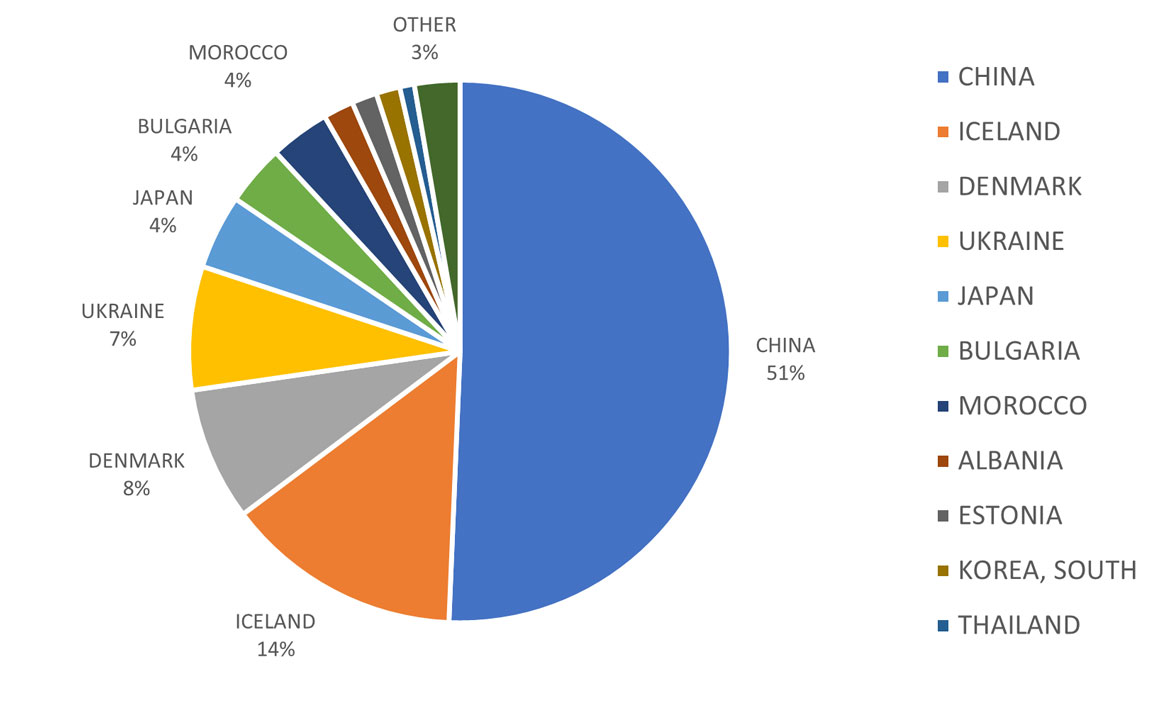

The offshore fleet focuses on a frozen at sea, shell-on product (cooked or raw). The product has major markets in Asia and Western Europe. In 2021, the export of Newfoundland and Labrador shell-on Northern shrimp product was 19.3 thousand tonnes valued at $124 million. The offshore fleet’s product was largely exported to China, Iceland and Denmark, accounting for 51 per cent, 14 per cent and 8 per cent respectively of Newfoundland and Labrador’s total frozen shell-on shrimp export value in 2021. For more information on Canadian exports of Northern Shrimp see Annex D (Figure 1).

1.6 Indigenous knowledge systems and contributions to the development of the rebuilding plan

DFO aims to weave Indigenous knowledge systems into fisheries management through Indigenous participation in the Northern Shrimp Advisory Committee (NSAC) (see IFMP Annex G). The Department holds dedicated advisory sessions for Indigenous partners ahead of, or following, the broader NSAC meeting which serves as a dedicated opportunity to gather Indigenous knowledge and perspectives.

More specifically in the development of this rebuilding plan, Indigenous partners with interest in the SFA 6 fishery were invited as members of the working group. A membership list for the SFA 6 Rebuilding Plan Working Group is at Annex E. Indigenous participation in the working group included Northern Coalition as a representative of some Indigenous licence holders as well as the Nunatsiavut Government. Further, under the Labrador Inuit Land Claims Agreement (LILCA), among other powers and responsibilities, the Torngat Joint Fisheries Board makes recommendations on the management of fisheries in the Labrador Inuit Settlement Area; and, may through advisory processes established by the Minister, advise on the conservation and management of fish in Waters Adjacent to the Zone (as defined in the LILCA). Where a portion of SFA 6 overlaps with Waters Adjacent to the Zone, the TJFB has advised and contributed as a member of the SFA 6 Rebuilding Plan Working Group. Innu Nation did not participate in the working group.

Where Northern shrimp is considered an offshore resource, there is no known record of harvesting the species under traditional methods that might contribute to stock assessment.

The Department is working on additional and/or alternative methods to weave Indigenous knowledge systems into fisheries management decision-making, as appropriate.

2.0 Stock status and stock trends

A PA framework including reference points to establish three stock status zones has been established for the stock, consistent with DFO’s Fishery Decision Making Framework Incorporating the Precautionary Approach. The USR defines the boundary between the Healthy and Cautious Zones, and represents a threshold for progressive reductions in the fishing mortality rate in effort to avoid the stock declining to its LRP. The LRP marks the boundary between the Cautious and Critical Zones. When a fish stock level falls below this point, there is a high probability that its productivity will be so impaired that serious harm will occur. The USR was defined as 80 per cent, and LRP as 30 per cent, of the geometric mean of the female SSB index over a productive period (1996-2003) (see section 1.4). These reference points have been used in assessments since 2010. The values of the PA reference points for SFA 6 were revised slightly in 2016 and again in 2018, in accordance with refinements in the biomass estimation method.

The status of Northern shrimp in SFA 6 is updated annually based on DFO fall multi-species trawl survey data. A summary of reference points is in Table 1, with further information related to the survey and stock assessment available at IFMP section 2.4.

| PA reference point | Stock-specific value of the reference point |

|---|---|

| Limit Reference Point (LRP) | 81,600 t |

| Upper Stock Reference (USR) | 218,000 t |

| Target Reference Point (TRP) | Not established. |

| Removal Reference (RR) | Not established. |

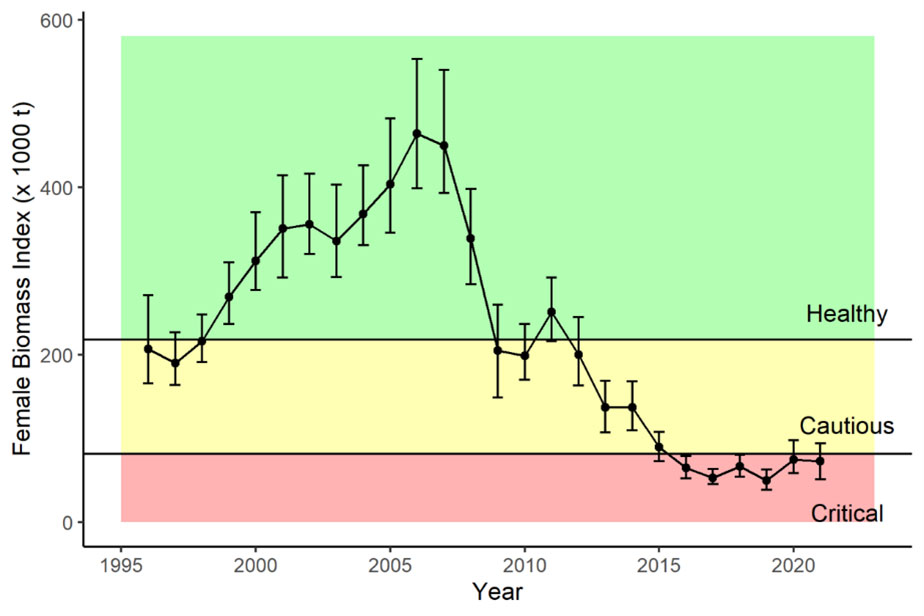

The 2016 survey showed the female SSB index enter the Critical Zone of the PA Framework for the first time (Figure 9). The stock assessment confirming the status of the stock in the Critical Zone occurred in February 2017Footnote 19. FB and female SSB indices remain amongst the lowest levels since the fall multi-species survey time series began in 1996.

Figure 9 - Text version

| Survey Year | Female SSB Biomass Index | Lower 95% CI Female | Upper 95% CI Female | LRP | USR |

|---|---|---|---|---|---|

| 1996 | 207 | 166 | 271 | 81600 | 218000 |

| 1997 | 190 | 164 | 227 | 81600 | 218000 |

| 1998 | 216 | 191 | 248 | 81600 | 218000 |

| 1999 | 269 | 237 | 310 | 81600 | 218000 |

| 2000 | 312 | 277 | 370 | 81600 | 218000 |

| 2001 | 351 | 292 | 414 | 81600 | 218000 |

| 2002 | 356 | 320 | 416 | 81600 | 218000 |

| 2003 | 336 | 293 | 403 | 81600 | 218000 |

| 2004 | 368 | 331 | 426 | 81600 | 218000 |

| 2005 | 404 | 346 | 482 | 81600 | 218000 |

| 2006 | 464 | 399 | 553 | 81600 | 218000 |

| 2007 | 450 | 393 | 540 | 81600 | 218000 |

| 2008 | 339 | 284 | 398 | 81600 | 218000 |

| 2009 | 205 | 149 | 260 | 81600 | 218000 |

| 2010 | 199 | 170 | 237 | 81600 | 218000 |

| 2011 | 251 | 216 | 292 | 81600 | 218000 |

| 2012 | 200 | 163 | 245 | 81600 | 218000 |

| 2013 | 137 | 107 | 169 | 81600 | 218000 |

| 2014 | 137 | 110 | 168 | 81600 | 218000 |

| 2015 | 89.6 | 72.9 | 108 | 81600 | 218000 |

| 2016 | 64.7 | 52.2 | 79.2 | 81600 | 218000 |

| 2017 | 52.7 | 45.3 | 63.6 | 81600 | 218000 |

| 2018 | 66.8 | 54.5 | 80.2 | 81600 | 218000 |

| 2019 | 49.9 | 38.5 | 63.1 | 81600 | 218000 |

| 2020 | 74.8 | 58.4 | 97.9 | 81600 | 218000 |

| 2021 | 72.9 | 51.1 | 94.2 | 81600 | 218000 |

The most recent assessment of Northern shrimp in SFA 6 occurred in February 2022 and considers 2021 fall multi-species survey data. The number of stations sampled by the DFO multi-species survey in 2021 had significant reductions. Simulated resampling of historic survey data, using 2021 survey coverage, suggest that the 2021 biomass estimates may slightly overestimate the stock status in SFA 6. Analysis of the 2021 survey data collected found FB and female SSB indices declined in 2021, by 20 per cent (to 94,300 t) and 3 per cent (to 72,900 t) respectively, and remain amongst the lowest levels in the post-1995 survey time series. The female SSB index is in the Critical Zone of the PA Framework for the sixth consecutive year, with a 22 per cent probability of being in the Cautious zone.

Despite the decline in FB and SSB indices from 2020 to 2021, analysis of recent stock trajectory shows a modest increase towards the LRP over the past three to five survey years. Further, trends in biomass indices show stability since entering the Critical Zone in 2017.

Further information on the most recent status of the stock is available in Science Advisory Report 2023/038. Due to the prioritization of comparative fishing work, a multi-species survey was not conducted in the Fall of 2022. For this reason, a 2023 stock assessment was not completed for Northern shrimp in SFAs 5 and 6. Decisions for the 2023-24 fishery considered previous science advice (Science Advisory Report 2023/038) as the best available information.

2.1 Committee on the Status of Wildlife in Canada (COSEWIC)

This stock has not been assessed by COSEWIC and is therefore not currently under consideration for listing under the Species at Risk Act (SARA).

3.0 Probable causes for the stock’s decline

3.1 Stock decline

There are indications that the shrimp biomass increased following the early 1990s collapse of groundfish predators. Shrimp per-capita net production (after factoring in natural mortality and fishing pressure) has declined since the mid-2000s. The decline in shrimp production has been associated with environmental conditions, increasing biomass of predatory fishes and commercial fishing. The warming trend in environmental conditions has had a negative impact on shrimp production. While currently water temperatures have returned to near their 1981-2010 average, statistical analyses suggest that the cumulative effects of past warmer conditions will likely continue to negatively affect shrimp stock production, and climate forecasts predict a continued long-term warming on the Newfoundland and Labrador shelfFootnote 20. The fishable biomass index is expected to remain low, or decline further, in the short term.

Given the relative impact of predation in recent years in SFA 6, small changes in catches from commercial fishing have the potential to be more influential on stock trajectory than they may have been in the mid-2000sFootnote 21.

3.2 Predation and prey considerations

In SFA 6, the total biomass of some groundfish that are known to prey on shrimp (e.g., Atlantic cod, Greenland halibut, redfish) has increased and consequently the amount of shrimp consumed by fish has also increased. Predation on shrimp, and the associated predation mortality rate, showed an increasing trend until 2011, and has decreased since then. The decrease is associated with an increase in consumption of capelin by predators in conjunction with the combined biomass of shrimp predators remaining relatively steady since 2011. The ratio between predation and shrimp biomass is a relative index of predation mortality and is currently around double the level in the mid-1990s and 2000s.

The trend in shrimp predation mortality in the near future appears highly associated with the availability of capelin as alternative prey. Capelin appears as a fundamental driver of groundfish rebuilding, while shrimp appears as an important food source for the subsistence of groundfish during low capelin periods. Shrimp predation mortality in the near future is expected to remain high unless abundance of alternative prey increases.

3.3 Habitat loss or degradation

Loss or degradation of the stock’s fish habitat is unlikely to have contributed to the stock’s decline based on the current understanding of the best available evidence.

4.0 Measurable objectives aimed at rebuilding the stock

4.1 Rebuilding target and timeline

4.1.1 Rebuilding target

The rebuilding target and primary objective of this rebuilding plan is to grow the female SSB above Brebuilt (B > Brebuilt), where Brebuilt is the female SSB estimated to be above the LRP with a minimum 75 per cent probabilityFootnote 22 (high likelihood).

Within the Critical Zone, this objective remains the same whether the stock is declining, stable, or increasing. This point signals the “end point” of the rebuilding plan, where management would transition back to the IFMP to continue the stock’s growth back to the Healthy zone.

4.1.2 Rebuilding timeline

A timeline to the rebuilding target is not feasible to establish for Northern shrimp in SFA 6 due to the inability to calculate Tmin or provide expert judgment as to generation time for the species. In accordance with Section 70(6) of the FGR, a rebuilding timeline has been omitted from the plan.

At this time, accurate ages for Northern shrimp cannot be determined. Estimates of when shrimp enter the fishery or mature as females (3-4 years) are available based on literature, but are not sufficient to provide generation time. Further, Northern shrimp abundances (FB, SSB, and total biomass) are highly variable year-to-year. No Northern shrimp stock (considering SFAs 4-6, EAZ or WAZ) has declined to the Critical Zone and rebuilt and thus could serve as reference for a possible timeline for rebuilding.

The Department continues to build its scientific knowledge on the stock in order to update stock status and provide science-based information on rebuilding timelines.

During each review of the rebuilding plan, DFO will examine whether a timeline to the rebuilding target can be calculated based on new information as it becomes available (see section 6.0).

4.2 Additional measurable objectives and timelines

Below is an overview of additional objectives for the Northern shrimp stock in SFA 6, relating to the categories of fisheries management, and knowledge gaps, and the associated timelines to achieve the objective. Objectives related to habitat restoration are not applicable where loss or degradation of the stock’s fish habitat is unlikely to have contributed to the stock’s decline.

Additional measurable objectives and timelines aimed at rebuilding the SFA 6 Northern shrimp stock.

- Rebuilding target - see section 4.1. Grow the female SSB above the LRP (B > Brebuilt), with a minimum 75 per cent probability.

Timeline: Timeline not possible to calculate at this time, see section 4.1. Advancements considered through CSAS peer-review stock assessment. - Develop a population assessment model capable of projecting changes in biomass.

Timeline: Model tentatively scheduled for CSAS peer-review in Fall 2024. - Concurrently review model- and empirical-based options for the LRP.

Timeline: Review of model- (and if necessary, empirical-) based LRP options tentatively scheduled for CSAS peer-review in Fall 2024. - Advance current scientific knowledge as it relates to connectivity of Northern shrimp in SFA 6 within a broader stock complex.

Timeline: Ongoing – advancements considered as part of the periodic review of the rebuilding plan, with contributions the tentative Fall 2024 CSAS peer-review. - Advance scientific temporal and spatial knowledge of Northern shrimp as a forage species, including its role in ecological relationships in a changing environment.

Timeline: Ongoing – advancements considered as part of the periodic review of the rebuilding plan.

5.0 Management measures aimed at achieving the objectives

Multiple management measures and/or departmental actions are required to achieve the objectives identified in section 4.2. These measures and expected outcomes are presented below.

Objective 1 - Grow the female SSB above the LRP (B > Brebuilt), with 75 per cent probability

- Management measure(s)

- TAC set to ensure the ER shall not exceed 10 per cent of the most recent estimate of FB.

- Section 8.0 further outlines scenarios for the review and potential modification of this management approach and anticipated timelines.

- Expected outcomes

- See below for section 5.1.

- Biology or environmental conditions taken into account

- This harvest decision rule considers that, under current ecosystem conditions, fishing at the current ER is unlikely to be a dominant driver for shrimp in SFA 6 as most available shrimp are likely consumed by predators.

- However; fishing, predation and warm climate conditions are all drivers of shrimp dynamics in this area and fishing pressure could now be more influential on stock trajectories than it may have been when the stock was large (i.e., in the mid-2000s)Footnote 23.

Objective 2 – Develop a population assessment model capable of projecting changes in biomass

- Management measure(s)

- Undertake applicable CSAS peer-review processes (PA Framework meeting tentatively scheduled for Fall 2024).

- Expected outcomes

- If a population projection model is successfully developed and accepted for use in future stock assessments, this will allow resource managers to predict the impacts of factors such as fishing pressure, as well as changing environmental and ecosystem conditions on future shrimp abundance.

- Biology or environmental conditions taken into account

- See section 1.2 – Environmental conditions and ecosystem factors affecting the stock.

Objective 3 – Concurrently review model- and empirical-based options for the LRP

- Management measure(s)

- Undertake applicable CSAS peer-review processes (PA Framework meeting tentatively scheduled for Fall 2024).

- Expected outcomes

- This will ensure resource managers are managing according to an LRP that most accurately reflects the point below which serious harm is occurring to the stock.

- Biology or environmental conditions taken into account

- See section 1.4 – Suitability of the LRP.

Objective 4 – Advance current scientific knowledge as it relates to connectivity of Northern shrimp in SFA 6 within a broader stock complex

- Management measure(s)

- Undertake applicable CSAS peer-review processes and collaborative efforts with industry, academics, and Indigenous partners.

- Expected outcomes

- This will promote a greater understanding of stock population dynamics and delineation, as well as increased knowledge of the influences of environmental and ecosystem conditions on shrimp abundance.

- Biology or environmental conditions taken into account

- See section 1.4 – Spatial scale of shrimp science assessment and management units.

Objective 5 – Advance scientific temporal and spatial knowledge of Northern shrimp as a forage species, including its role in ecological relationships in a changing environment

- Management measure(s)

- Undertake applicable CSAS peer-review processes and collaborative efforts with industry, academics, and Indigenous partners.

- Expected outcomes

- This will promote a greater understanding of Northern shrimp’s relationship with key commercial predator species on temporal and spatial scales, particularly in the context of changing environmental conditions.

- Biology or environmental conditions taken into account

- See section 1.2 – Environmental conditions and ecosystem factors affecting the stock.

5.1 Discussion of management measures – Fishery controls

Consistent with DFO’s 2009 PA Policy, while the stock is in the Critical Zone, management actions must promote stock growth, removals from all sources must be kept to the lowest possible level, and there should be no tolerance for preventable decline.

The most recent stock assessment (2022) concluded that under current ecosystem conditions, fishing is unlikely to be a dominant driver of shrimp stocks in SFA 6 but that fishing pressure could now be more influential on stock trajectories than it may have been in the pastFootnote 24. While fishing remains a driver of shrimp dynamics, among other factors, the exact level of fishing that would be consistent with rebuilding the stock remains especially uncertain in the absence of a projection model.

Stock trajectory under a maximum 10 per cent ER (actual ER ranging from 7.56 to 9.97 per cent) shows a modest increase towards the LRP over the past three to five surveys from 65 per cent of the LRP to 91 per cent in the 2017 survey, and to 88 per cent in the 2021 survey. This could suggest that continued management under this approach is not likely to hinder rebuilding efforts in the short term. It is acknowledged that uncertainty in the FB index, to the extent an overestimation may have occurred, could influence our understanding of stock trajectory.

As a maximum, this approach maintains Minister discretion to consider TAC levels based on an ER less than 10 per cent, especially where the most recent science advice might signal a need to reduce exploitation to promote rebuilding.

This rebuilding plan outlines an explicit workplan to develop a population assessment model and review model-based options for the LRP in the near term (objectives 2 and 3). This workplan will ensure the stock is being managed according to an LRP that most accurately reflects the point below which serious harm is occurring to the stock, and will inform selection of management measures best suited to promote stock growth. Should a model not be successfully developed, the rebuilding plan includes a contingency means to review the LRP to inform future management.

Objectives 2 and 3 underline the interim nature of this rebuilding plan and its management measures, until such time as new information can guide changes to this approach.

6. Socio-economic analysis

Section 1.5 of this document presented the socio-economic profile of the SFA 6 Northern shrimp fishery, including the discussion on dependency ratios. The management measures under this rebuilding plan will not result in any changes to the setting of annual quotas (based on a maximum 10 per cent ER) and does not propose changes to the sharing key by fleet/interest (inshore, offshore, special allocations). Thus, this rebuilding plan is not expected to have any incremental socio-economic impacts to harvesters, processors, indigenous communities or the local economy.

7. Method to track progress towards achieving the objectives

Performance metrics provide DFO with a means to assess the progress of the rebuilding plan towards the plan’s objectives. Below is a summary of the performance metrics and frequency of measurement associated with each objective in this rebuilding plan.

Objective 1 - Grow the female SSB above the LRP (B > Brebuilt), with 75 per cent probability

- Metric to measure Progress

- FB and SSB indices from fall multi-species survey. SSB considered relative to Brebuiltwith a minimum 75 per cent confidence.

- Frequency of Measurement

- Stock status updated through CSAS stock assessment or update.

Objective 2 – Develop a population assessment model capable of projecting changes in biomass

- Metric to measure Progress

- Model is approved for use in management decision-making; DFO approved products/outcomes made publicly available (e.g., DFO Science technical brief, CSAS publication).

- Frequency of Measurement

- Once.

Objective 3 – Concurrently review model- and empirical-based options for the LRP

- Metric to measure Progress

- DFO approved products/outcomes made publicly available (e.g., DFO Science technical brief, peer-reviewed CSAS publication).

- Frequency of Measurement

- Once.

Objective 4 – Advance current scientific knowledge as it relates to connectivity of Northern shrimp in SFA 6 within a broader stock complex

- Metric to measure Progress

- DFO approved products/outcomes made publicly available (e.g., DFO Science technical brief, peer-reviewed CSAS publication).

- Publication of relevant peer-reviewed and grey literature.

- Frequency of Measurement

- Ongoing – advancements considered as part of the periodic review of the rebuilding plan.

Objective 5 – Advance scientific temporal and spatial knowledge of Northern shrimp as a forage species, including its role in ecological relationships in a changing environment

- Metric to measure Progress

- DFO approved products/outcomes made publicly available (e.g., DFO Science technical brief, peer-reviewed CSAS publication).

- Publication of relevant peer-reviewed and grey literature.

- Frequency of Measurement

- Ongoing – advancements considered as part of the periodic review of the rebuilding plan.

8. Periodic review of the rebuilding plan

The department will engage stakeholders on any matter related to the implementation / review of the rebuilding plan through the established NSAC process. The SFA 6 Rebuilding Plan Working Group (Annex E) will act as a monitoring body to this plan in addition to NSAC, and will continue to convene as required to address any aspect of the rebuilding plan in the short and long term.

Where success of objectives 2 and 3 of this rebuilding plan would have direct implications on management measures currently identified in the plan, a review would be conducted in the following related circumstances (see objectives and timelines in section 4.2):

- The availability of a peer-reviewed and accepted population model to inform management;

- The establishment of a revised LRP.

Notwithstanding the circumstances above, a periodic review of the plan will occur every three years (i.e., following every three stock assessments) to determine whether progress towards the plan’s objectives, including the rebuilding target, is being made and whether revisions to the rebuilding plan are necessary in order to achieve those objectives. This interval is considered a reasonable timeframe in which new scientific information and advancements to address knowledge gaps is likely to become available. This includes information available to support the establishment of a rebuilding timeline. Additional reviews may also be conducted outside this schedule due to any other exceptional circumstance that warrants a review of the rebuilding plan.

The review will be based on the data gathered using the metrics identified in the “Method to Track Progress Towards Achieving the Objectives” section of this plan. It will assess the progress of the implementation of management measures and evidence of their effectiveness, as well as the status of the stock and recent trends. In addition, the review will include opportunities for consultation with Indigenous groups and stakeholders on their views of the stock’s progress towards rebuilding.

The review process will generate a report that evaluates progress towards each management objective against their timelines with accompanying evidence and may propose adjustments to the rebuilding plan if necessary to achieve the objectives.

Stock rebuilding is not always a slow and steady, or even predictable process. Stocks may fluctuate and/or persist at low levels for years until conditions promote surplus production, resulting in rapid growth of the population. Thus, lack of progress towards rebuilding may not be an indication that the rebuilding plan’s objectives or management measures are insufficient or ineffective.

9. References

Carruthers, E., Parlee, C., Keenan, R., and Foley, P. 2019. Onshore benefits from fishing: Tracking value from the Northern Shrimp fishery to communities in Newfoundland and Labrador. Marine Policy, Volume 103, 2019, Pages 130-137, ISSN 0308-597X.

DFO. 2009. Proceedings of the Precautionary Approach Workshop on Shrimp and Prawn Stocks and Fisheries; November 26-27, 2008. DFO Can. Sci. Advis. Sec. Proceed. Ser. 2008/031

DFO. 2017a. Review of Reference Points used in the Precautionary Approach for Northern Shrimp (Pandalus borealis) in Shrimp Fishing Area 6. DFO Can. Sci. Advis. Sec. Sci. Resp. 2017/009.

DFO. 2017b. An assessment of Northern Shrimp (Pandalus borealis) in Shrimp Fishing Areas 4– 6 and of Striped Shrimp (Pandalus montagui) in Shrimp Fishing Area 4 in 2016. DFO Can. Sci. Advis. Sec. Sci. Advis. Rep. 2017/012.

DFO. 2018a. An assessment of Northern Shrimp (Pandalus borealis) in Shrimp Fishing Areas 4-6 in 2017. DFO Can. Sci. Advis. Sec. Sci. Advis. Rep. 2018/018.

DFO. 2018b. Northern shrimp and striped shrimp - Shrimp fishing areas 0, 1, 4-7, the Eastern and Western Assessment Zones and North Atlantic Fisheries Organization (NAFO) Division 3M. Integrated Fisheries Management Plans (IFMP). Fisheries Resource Management, Fisheries and Oceans Canada.

DFO. 2022a (Preliminary). Integrated Catch and Effort System [database]. Ottawa.

DFO. 2023. Assessment of Northern Shrimp (Pandalus borealis) in Shrimp Fishing Areas 4-6 in 2021. DFO Can. Sci. Advis. Sec. Sci. Advis. Rep. 2023/038.

Jorde, P.E., Søvik, G., Westgaard, J.I., Orr, D., Han, G., Stansbury, D., and K.E. Jørstad. 2014. Genetic population structure of Northern Shrimp, Pandalus borealis, in the Northwest Atlantic. Can. Tech. Rep. Fish. Aquat. Sci. 3046: iv + 27 p.

Koen-Alonso, M., and Cuff, A. 2018. Status and trends of the fish community in the Newfoundland Shelf (NAFO Div. 2J3K), Grand Bank (NAFO Div. 3LNO) and Southern Newfoundland Shelf (NAFO Div. 3Ps) Ecosystem Production Units. NAFO SCR Document, 18/070: 1-11.

Le Corre, N., Pepin, P., Han, G., Ma., Z., and P.V.R. Snelgrove. 2019. Assessing connectivity patterns among management units of the Newfoundland and Labrador shrimp population. Fisheries Oceanography FOG-18-1441.

Le Corre, N., Pepin P., Burmeister A., Walkusz W., Skanes K., Wang Z., Brickman D., Snelgrove P.V.R. 2020. Larval connectivity of Northern Shrimp (Pandalus borealis) in the Northwest Atlantic. Canadian Journal of Aquatic and Fisheries Sciences. DOI: 10.1139/cjfas-2019-0454.

Le Corre, N, Pepin, P, Han, G, Ma, Z. Potential impact of climate change on Northern Shrimp habitats and connectivity on the Newfoundland and Labrador continental shelves. Fish Oceanogr. 2021; 30: 331–347.

NAFO. 2021. Report of the 14th Meeting of the NAFO Scientific Council Working Group on Ecosystem Science and Assessment (WG-ESA). NAFO SCS Doc. 21/21, Serial No. N7256, 181 pp. pages 141 - 157.

Pedersen, E.J., Skanes, K., le Corre, N., Koen Alonso, M., and Baker, K.D. 2022. A New Spatial Ecosystem-Based Surplus Production Model for Northern Shrimp in Shrimp Fishing Areas 4 to 6. DFO Can. Sci. Advis. Sec. Res. Doc. 2022/062. v + 64 p.

Annex A: History of TAC levels and catch in SFA 6 (2013/2014-2022/2023)

| - | 2013-14 Initial |

2014-15 Initial |

2015-16 Initial |

2016-17 Initial |

2017-18 Initial |

2018-19 Initial |

2019-20 Initial |

2020-21 Initial |

2021-22 Initial |

2022-23 Initial |

|---|---|---|---|---|---|---|---|---|---|---|

| Offshore fleet (includes SABRI, FOGO & Innu allocations) |

18,952 | 16,559 | 16,559 | 8,459 | 3,161 | 2,654 | 2,724 | 2,520 | 2,898 | 2,867 |

| Inshore fleet | 41,293 | 31,637 | 31,637 | 19,366 | 7,239 | 6,076 | 6,236 | 5,770 | 6,636 | 6,563 |

| Total | 60,245 | 48,196 | 48,196 | 27,825 | 10,400 | 8,730 | 8,960 | 8,290 | 9,534 | 9,430 |

| - | 2013-14 Catch |

2014-15 Catch |

2015-16 Catch |

2016-17 Catch |

2017-18 Catch |

2018-19 Catch |

2019-20 Catch |

2020-21 Catch |

2021-22 Catch |

2022-23 Catch |

|---|---|---|---|---|---|---|---|---|---|---|

| Offshore fleet (includes SABRI, FOGO & Innu allocations) |

18,284 | 13,602 | 17,344 | 7,513 | 3,246 | 2,665 | 2,705 | 2,714 | 2,831 | 2,900 |

| Inshore fleet | 40,550 | 28,506 | 31,378 | 17,630 | 6,819 | 6,038 | 5,933 | 3,553 | 6,750 | 5,398 |

| Total | 58,834 | 42,108 | 48,722 | 25,143 | 10,065 | 8,702 | 8,638 | 6,267 | 9,581 | 8,297 |

Annex B: History of northern shrimp fishery

1970s to 1997

The Northern shrimp fishery began in the early to mid-1970s following exploratory cruises by DFO that confirmed the presence of shrimp in the waters from Baffin Island southward to Newfoundland and Labrador (NL). By the late 1970s, four Canadian companies operating from vessels greater than 100 feet were licensed to prosecute the fishery under cooperative arrangements to determine the commercial feasibility of harvesting. It should be noted that the risk and cost associated with developing this fishery during the initial stages was high and some licence holders used foreign vessels to harvest shrimp allocations.Footnote 25 At that time, the fishery was largely concentrated in three areas – the Davis Strait (NAFO Division 0A); Hopedale Channel (2H), and Cartwright Channel (2J), with landings occurring in the Maritime provinces, Quebec and NL. Historical reports from the NL Region indicate that, in 1978, Northern shrimp landings accounted for around one per cent of the total volume of all fish landings, which largely comprised groundfish and pelagics.Footnote 26

In 1986, the Total Allowable Catch (TAC) in Hopedale Channel was set at 3,400 t.Footnote 27 The TAC was harvested, and based on historical data in the NL Region, this volume would have had a landed value of about $4 million. Five vessels, four domestic and one foreign participated in the fishery, which began in the last week of June and continued until late November when the area closed. Fishing in Cartwright Channel did not begin until after the closure of Hopedale Channel. Four vessels, two domestic and two foreign, reportedly harvested the 1,000 t TAC and fishing in this area continued into the new year. There was no fishery in the Hawke Channel (2J) or in 3K; however, a winter fishery occurred in these areas, with reported landings of about 800 t and 50 t, respectively.

In the ensuing years, a growing market demand led to higher prices and a significant increase in Northern shrimp landings.Footnote 28 Furthermore, fleet expansion and improvements in fishing gear, coupled with the implementation of the Enterprise Allocation (EA) system, led to more efficient utilization of resources.Footnote 29 Around this time, the fishery also adopted a Shrimp Fishing Area (SFA) management approach. Under this system, each licence holder received an equal enterprise allocation within each SFA. As a result, by the late 1980s, the Northern shrimp fishery had developed into a substantial industry with capital-intensive investments in modern freezer trawlers and annual landings of over 26,000 t. Historical reports indicate that the industry directly employed about 600 people and had a total landed value of approximately $100 million. The relative size of the fishery compared to other commercial fisheries was also increasing. For example, in the NL Region, Northern shrimp increased from 2 per cent of the total landed value of all species harvested in 1986 to 15 per cent in 1988.

Landings from the Hawke Channel, located in Shrimp Fishing Area (SFA 6), were also increasing. Expansion of the fishery into this more southerly SFA allowed the greater than 100 feet fleet to operate close to year-round, thereby improving its economic performance. At that time, Northern shrimp landings were well distributed across all SFAs, and with landings increasing from SFA 6, the fishery had become a world-class supplier of cold-water shrimp. In 1991, a total of 17 greater than 100 feet licenses had been issued, and by 1996, the TAC for Northern shrimp was 37,600 t, of which SFA 6 accounted for 11,050 t or 29 per cent.

It is important to recognize that, since the late 1970s, the Northern shrimp fishery has included licences held by Indigenous birthright corporations and other community-based organizations owned predominately by Indigenous peoples. Beneficiaries of these licences included residents of Labrador, Quebec, and Nunavut. The revenue generated from this access, whether through direct fishing or royalty charter arrangements, has contributed to economic development and employment within these communities. For instance, the Northern Coalition, a non-profit organization of Indigenous and community enterprises promoting sustainable and equitable fishing in Northern regions, publicly reports that it reinvests all profits and revenues from Northern shrimp licences into approximately 45 social enterprises across more than 50 Northern coastal communities.

Introduction of new fishery participants (1997)

Following the decline of groundfish and the subsequent moratoria of the early 1990s, colder waters and fewer groundfish predators contributed to significant growth in the Northern shrimp resource, particularly in more southerly SFAs. By 1997, 367 temporary permits were issued to eligible inshore (at the time those 40 to 65 feet) fishing enterprises based in NAFO Divisions 2J, 3KL, 4R and 4S, and their access was limited to SFA 6, and later extended to SFA 7.Footnote 30 Up to this time, Northern shrimp was almost exclusively landed as a frozen-at-sea product by the greater than 100 feet fleet. The introduction of inshore fishing enterprises was the beginning of the cooked and peeled shrimp industry, which entailed inshore vessels landing wet to onshore production facilities. The expansion of this industry resulted in a new source of fishing revenue for eligible inshore fishing licence holders and crew. It also led to new jobs for onshore plant workers and other service industries. At its peak, there were 13 onshore shrimp processing plants in NL, employing approximately 2,000 plant workers. This new fishery provided an infusion of economic activity in some rural areas that had been negatively impacted by the groundfish moratoria.

In addition to the inshore shrimp fleet, access to Northern shrimp was also granted to “special allocations.” Special allocations comprised organizations, communities or entities, including Indigenous organizations, that received an allocation for their economic benefit. Access to special allocation holders was granted in most SFAs, and these allocations were typically harvested by the greater than 100 feet fleet under royalty charter arrangements. By 2000, there were a total of five special allocation holders in SFA 6. However, as the resource declined, some of these were removed from the fishery in conjunction with the Last In, First Out (LIFO) policy.Footnote 31 Currently, there are three special allocation holders in SFA 6 – St. Anthony Basin Resources Inc. (SABRI), the Innu Nation and the Fogo Island Cooperative. Understanding the importance of shrimp to these groups hinges on available information. In that respect, such information is more readily available from SABRI and is included here for additional context.

In 1997, SABRI received a special allocation of 3,000 t of Northern shrimp to benefit 16 communities on the Northern Peninsula of NL. Over the years, SABRI has reportedly reinvested these royalties to support the local economy and job market. In addition to several other initiatives, SABRI has made significant investments in the port of St. Anthony, including the construction of a cold storage facility. SABRI maintains a 4.5 per cent quota share of the SFA 6 TAC. The Innu Nation and Fogo have quota shares of 1.7 per cent and 1.1 per cent, respectively.

Post 1997

The Northern shrimp TAC in SFAs 0 to 7 continued to increase, and by 2008-09, it had peaked at about 177,000 t, of which the SFA 6 quota accounted for about 85,725 t, or close to 50 per cent. Total Northern shrimp landings in 2008, all fleets and SFAs, amounted to approximately 135,000 t with a total landed value of about $250 million. By comparison, SFA 6 shrimp landings in 2008 totaled about 75,000 t, or 55 per cent of total Northern shrimp landings. The SFA 6 landed value of approximately $110 million accounted for about 44 per cent of total Northern shrimp landed value.

Subsequent to 2008, the SFA 6 shrimp quota started to decline, and by 2015, it was 48,196 t, about a 44 per cent reduction over that seven year period. Furthermore, the SFA 7 fishery was closed to directed fishing in 2015. However, SFA 6 continued to be a significant fishing area, with a quota accounting for about 43 per cent of the total Northern shrimp TAC (all SFAs). Despite the quota reduction, in 2015, the SFA 6 fishery had a landed value of about $190 million, largely due to higher landed prices. In the NL Region, the landed value of SFA 6 shrimp accounted for approximately 22 per cent of the total landed value of all species harvested.

It should be noted that the tremendous growth in SFA 6, and subsequently SFA 7, quotas was not without its challenges (e.g., underutilized capacity, quality, seasonality; etc.). Over the years, there have been a number of studies by government to review the cooked and peeled shrimp industry with a view to recommending ways to improve efficiency and cost effectiveness in the industry.Footnote 32 Since 2008, DFO has implemented policy changes to allow for industry self-rationalization in the inshore fleet. This has resulted in a significant reduction in the number of SFA 6 inshore shrimp licences, from about 367 to approximately 203. As the quota declined, the number of shrimp processing plants in NL has also been reduced to about six at present. For the greater than 100 feet fleet, quota reductions in SFA 6 have also impacted their year-round operations since, for a portion of the year, the northern SFAs have heavy ice coverage.

In 2022, the SFA 6 shrimp quota was 9,430 t and accounted for about 12 per cent of the total Northern shrimp TAC. This is a decline of close to 90 per cent, or about 76,000 t, from the peak of 2008-09. Total SFA 6 landings were about 8,600 t, with a total landed value of about $30 million. In NL Region, the total landed value of SFA 6 Northern shrimp comprised about 2 per cent of the total landed value of all species harvested. It is important to note that these figures reflect the direct impact from fishing revenue.

Beyond this, the SFA 6 Northern shrimp fishery continues to generate indirect and induced impacts that support employment and related economic activity. For example, in addition to revenues and employment through onshore processing activities and offloading/transshipment, the Northern shrimp fishery supports other sectors such as trucking, vessel repair, gear suppliers and general retail, among others. These related sectors benefit from direct expenditures by inshore enterprises and offshore companies, and from demand created by harvesting and processing. Municipalities are responsible for providing a broad range of services to residents, including road repair, water and sewage systems, garbage collection, fire services and snow clearing. To pay for these services, municipal budgets in communities across NL, particularly rural NL, depend to varying degrees on tax revenues derived from harvesting and processing (for example, processing plants).Footnote 33

Annex C: Dependency analysis

| Fishing Revenue Dependency on SFA 6 Northern Shrimp (in per cent) | # of Enterprises | Average Landed Value of SFA 6 Northern Shrimp | Total Landed Value of SFA 6 Northern Shrimp3 | Average Landed Value of All Species in All Areas | Total Landed Value of All Species in All Areas4 | Average Fishing Revenue Dependency on SFA 6 Northern Shrimp5 (in per cent) |

|---|---|---|---|---|---|---|